The crisis enters its third year

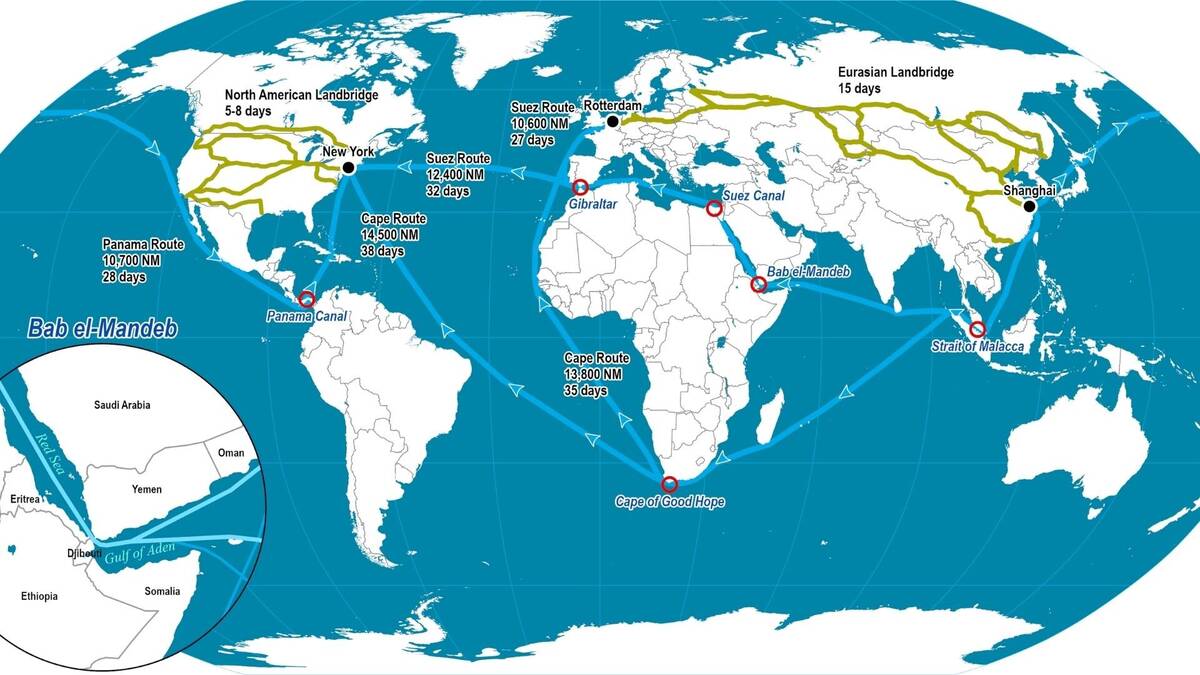

Since November 2023, Houthi militants based in Yemen have carried out more than 190 attacks on commercial shipping vessels transiting the Red Sea and Bab el-Mandeb Strait. This strategic waterway connects the Suez Canal to the Indian Ocean and typically handles 12 to 15 percent of global maritime trade.

The attacks forced major shipping lines including Maersk, MSC, CMA CGM, and Hapag-Lloyd to reroute vessels around Africa's Cape of Good Hope, adding approximately 3,500 nautical miles and 10 to 14 days to Asia-Europe transit times. Container ship transits through the Suez Canal plummeted by 90% compared to pre-crisis levels.

2026: a brief hope and renewed disruption

Early 2026 saw cautious optimism as carriers began testing limited returns to the Suez Canal following a ceasefire between Hamas and Israel. Maersk announced a full return to Red Sea transits, and several carriers rerouted selected services through the canal.

However, US and Israeli military operations against Iran in late February 2026 shattered these hopes. Houthi commanders threatened renewed attacks on commercial shipping, and carriers immediately reversed their Suez Canal decisions. CMA CGM suspended all Suez transits and rerouted via the Cape of Good Hope. The Gemini Cooperation reversed its Red Sea return. All major carriers issued advisories prioritizing crew and cargo safety.

Impact on freight rates

The crisis has kept freight rates elevated compared to pre-disruption levels, though market dynamics have created complex pricing patterns. Spot rates from China to North Europe remain approximately 48% above pre-crisis levels. Rates from China to the Mediterranean are still 79% higher than December 2023. Transpacific rates have been less affected but still show elevated premiums for schedule reliability.

The longer routes mean carriers need more vessels to maintain the same service frequency, absorbing capacity that would otherwise create overcapacity and drive rates lower. When carriers briefly returned to the Suez Canal, the market anticipated rate declines, but the renewed disruptions have stabilized rates at moderately elevated levels.

Impact on transit times

For shippers, the most tangible impact is on transit times. Asia to Europe shipments now take approximately 40 to 45 days via the Cape of Good Hope compared to 25 to 30 days through the Suez Canal. This adds two to three weeks to supply chain lead times, increases inventory carrying costs, and requires earlier ordering and larger safety stock.

War risk insurance

Insurance premiums for vessels transiting the Red Sea have increased substantially. Many insurers now require separate war risk policies with premiums that can add $100,000 to $500,000 per voyage. These costs are ultimately passed through to shippers as surcharges.

What shippers should do

Build longer lead times into your supply chain planning, assuming Cape of Good Hope routing as the baseline. Increase safety stock to buffer against transit time variability. Negotiate contracts with flexibility for route changes and transit time adjustments. Consider air freight for time-critical shipments where the economics justify the premium. Diversify sourcing to reduce dependence on trade lanes most affected by the crisis. Monitor developments closely, as the situation can change rapidly.

How ASR navigates the crisis for clients

We actively monitor the Red Sea situation and adjust routing recommendations for our clients. Our ocean freight team provides real-time updates on carrier schedules, rate changes, and transit time estimates. Contact us for a supply chain risk assessment at shipping@asrwe.com or +1 786 373 3003.