The 2026 ocean freight landscape

The ocean freight market in 2026 is shaped by competing forces that make forecasting unusually challenging. On one side, massive fleet growth continues to inject new capacity into the market. On the other, geopolitical disruptions and trade policy shifts keep routing unpredictable and capacity management complex.

Understanding these dynamics is essential for any shipper planning their logistics budget and contract negotiations.

Key factors driving rates

Fleet overcapacity

The global container fleet continues to grow faster than demand. Capacity increased by 7% in 2025 and is expected to grow another 3.7% in 2026, adding approximately 1.5 million TEUs. Even larger growth of 8% is projected for 2027 as new vessel orders from the ordering boom of 2021-2022 continue to deliver.

Under normal circumstances, this overcapacity would push rates significantly lower. However, the Red Sea crisis has absorbed much of this excess capacity by keeping vessels on longer routes around Africa.

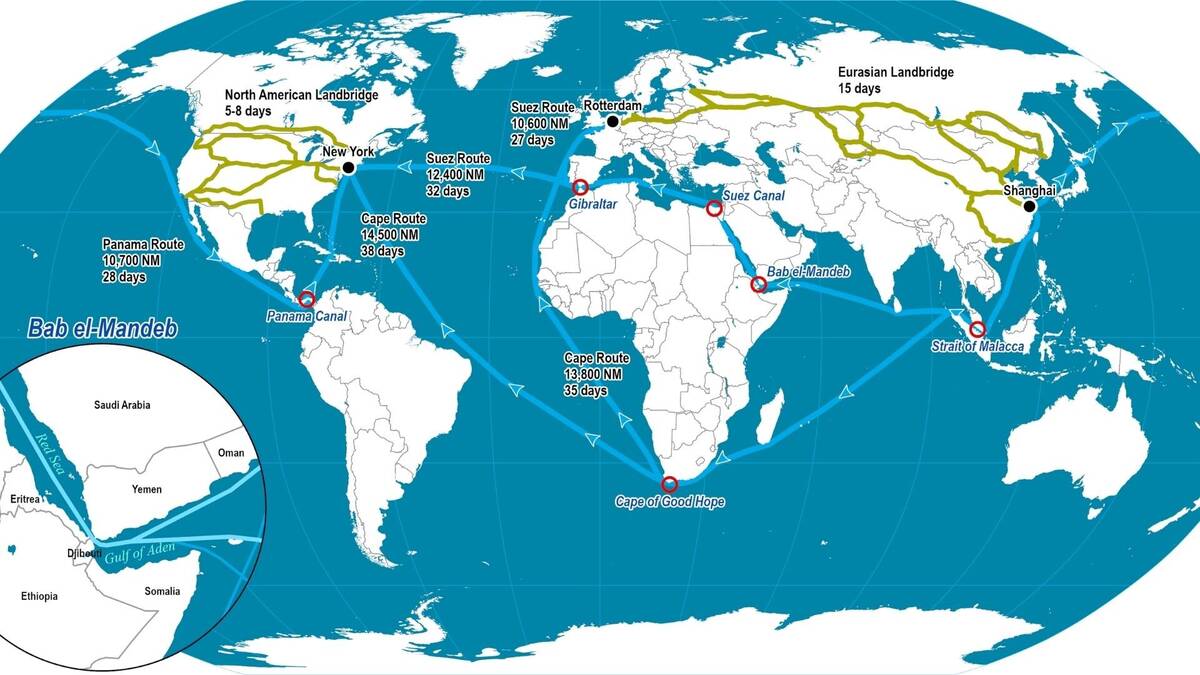

Red Sea diversions

The continued rerouting of vessels around the Cape of Good Hope effectively removes approximately 6% of global vessel capacity from the market. If carriers fully return to the Suez Canal, this capacity would flood back into the market almost overnight, creating intense downward pressure on rates.

Trade policy uncertainty

US tariff policy has created unusual demand patterns. The frontloading phenomenon of 2025, where importers rushed to ship goods ahead of tariff increases, pulled demand forward and created an artificial volume spike. The payback period in 2026 is expected to suppress volumes as importers work through excess inventory.

Demand outlook

Global container volumes are expected to grow modestly in 2026, though US import volumes may contract by approximately 2% as tariff costs impact consumer spending and importer decisions. Growth in other markets, particularly intra-Asia and emerging market trade, partially offsets this decline.

Rate forecast by trade lane

Transpacific (Asia to US)

Contract rate negotiations for 2026 are expected to favor shippers, particularly on eastbound transpacific lanes. Overcapacity and subdued US demand should keep rates competitive. Spot rates from China to the US West Coast have already fallen 35% since the start of 2026. East Coast rates are down approximately 32%.

Asia to Europe

This trade lane is most directly affected by the Red Sea crisis. Rates remain elevated but are trending downward. A full return to the Suez Canal would trigger significant rate declines, though the current geopolitical situation makes this unlikely in the near term.

Intra-Asia

Intra-Asia trade lanes continue to show stable to moderate growth, benefiting from supply chain diversification as manufacturers shift production within the region.

Strategies for shippers

Lock in favorable contract rates during the current soft market, particularly on transpacific lanes. Split volume between contract and spot exposure to take advantage of market dips. Build flexibility into contracts with volume swing provisions and multiple routing options. Monitor the Red Sea situation closely, as a return to Suez transits would significantly impact rates.

Partner with ASR for ocean freight

Our ocean freight team monitors market conditions daily and advises clients on optimal timing for rate negotiations, carrier selection, and routing decisions. Whether you ship FCL or LCL, we help you get competitive rates while maintaining schedule reliability. Request a rate quote at asrwe.com/quote or contact us at shipping@asrwe.com.